Middle East Can Lead the Next Decade of Digital Commerce

The Middle East is entering a defining decade. As artificial intelligence, climate risk and shifting trade patterns redraw the global growth map, value is literally in motion.

The Middle East is set to Lead the Next Decade of Digital Commerce.

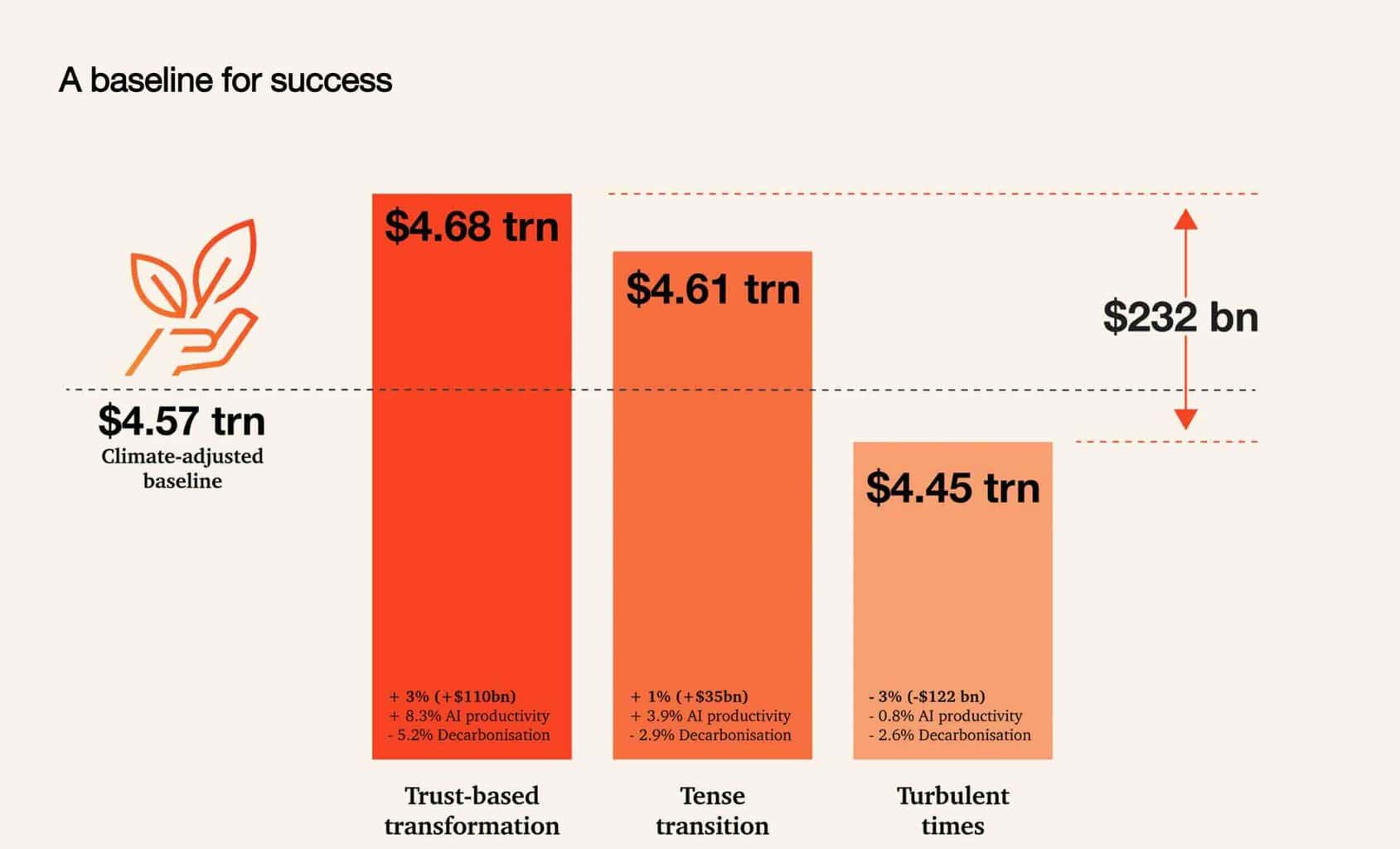

The Middle East is entering a defining decade. As artificial intelligence, climate risk and shifting trade patterns redraw the global growth map, value is literally in motion. PwC’s new analysis quantifies the stakes; by 2035, the region’s climate-adjusted baseline points to $4.57 trillion in GDP, yet outcomes range from $4.45 trillion in a fractured world to $4.68 trillion if trust in AI and climate execution aligns. That $232 billion gap is not academic; it is the difference between a defensive posture and a confident export of standards.

Two forces dominate the calculus. First, if scaled responsibly, AI productivity can add 8.3 percentage points to regional GDP by 2035. Second, physical climate risks, such as extreme heat, water stress and flooding, can subtract 13.9 points if unmanaged. In practical terms, the region’s growth will be set by how quickly it converts cheap, clean power into cheap, abundant compute, and how effectively it uses that compute to raise productivity while hardening supply chains against climate impacts.

This is where the Middle East holds a structural advantage. The Gulf’s world-class renewable resources, falling levelised electricity costs, and rapid buildout of data centre capacity translate into lower marginal costs for AI training and inference. Pair that with policy plumbing, real-time payments, open-banking frameworks, and e-invoicing, and you get retail rails that turn connectivity into checkout. These rails are not headlines, but they are the difference between campaigns that fade and customers who return.

PwC’s framing is helpful because it moves beyond sectors to growth domains. Instead of treating retail as an island, it sits at the intersection of Connect & Compute (search, recommendations, payments), Move (fulfilment and returns), and Fund & Insure (working capital, risk, buyer protection). That is precisely where e-commerce will be won in MENA; in the seams between discovery, money movement and delivery.

The signals are already visible. Internet penetration is effectively universal in Gulf markets, mobile speeds are world-class, and national real-time payment systems have gone mainstream. E-invoicing has cleaned up data and accelerated settlements. Open-banking is shifting from pilots to production, enabling account-to-account checkout that lowers fees and raises approvals. Meanwhile, Arabic-first search, service and pricing models are moving from proof-of-concept to production. This matters because the next wave of retail growth comes from relevance at the edge, localised content, accurate attributes and trustworthy service, not just more ads.

The region also has momentum in cross-industry plays, super-apps expanding from mobility to delivery and payments, AI-driven healthcare platforms merging clinical capacity with data science, and energy incumbents investing in electric vehicles and storage. These moves preview the new value chains that commerce will plug into faster identity verification at checkout, cleaner returns logistics, and more predictable cash cycles for sellers.

Our view is unapologetically operational. If the Middle East chooses the trust-based transformation track, the winners will be operators who standardise four things across borders:

-

Checkout that works: Card + pay-by-bank + strong identity. Raise approvals, cut false declines, and shorten settlement—this is free growth.

-

Product data that converts: Arabic-first titles and attributes, richer media, accurate sizing. This lowers avoidable returns.

-

Delivery promises that hold: Honest two-day nationwide targets with precise refund clocks and drop-off options. Trust is logistics you can keep.

-

Clean compliance: Predictable VAT, e-invoice, and product-safety playbooks. Less drama, faster scale.

There are risks. Talent gaps in growth operations persist; many SMEs still run on spreadsheets; and return rates can quietly crush margins. But these are execution problems, not structural weaknesses, and are solvable on the rails that Gulf regulators and infrastructure investors are building.

The strategic choice is clear. AI needs watts; watts are cheap here. If the region uses that advantage to power local, explainable, and trustworthy retail AI and exports the standards for payments, invoicing, and returns across the GCC, it will not only capture the high end of PwC’s range; it will set the playbook others adopt. That is how a region moves from being a place where value flows to being a place that defines how value flows.

For marketplaces, brands, logistics, and payment firms and the investors who back them, the task is to treat these next five years as an installation window, installing the rails, the trust, and the talent. The prize is not simply higher GMV; it is a durable customer base and an exportable model of digital trade built on clean energy and credible AI.

The bottom line is that the Middle East’s time to lead is not a slogan but a cost curve plus a policy stack. Turn both into everyday checkout, and the region’s value in motion becomes value captured.